![FortnightlyReport]()

24 July 2019

21 Tammuz 5779

21 Dhul Qadah 1440

TOP STORIES

TABLE OF CONTENTS:

1: ISRAEL GOVERNMENT ACTIONS & STATEMENTS

1.1 Israel Launches Cybersecurity Program for Students with Communications Disorders

1.2 Tel Aviv Residents Appeal to Municipality to Require Permits for Airbnb Operators

1.3 Verkhovna Rada Ratifies Free Trade Agreement Between Ukraine and Israel

2: ISRAEL MARKET & BUSINESS NEWS

2.1 Israeli Defense Companies Team with Lockheed Martin to Enter the US Market

2.2 YL Ventures Closes Fourth Fund with $120M of Committed Capital

2.3 enSilo Raises $23 Million in Series B Funding

2.4 Juganu Raises $23 Million led by Viola Growth

2.5 Eyesight Partnering With Leading Tier 1 to Continue Leadership in Chinese Market

2.6 Israel Enters Top 10 Most Innovative Nations in UN’s WIPO Index

2.7 UVeye Raises $31 Million from Volvo Cars, Toyota Tsusho and W.R. Berkley

2.8 The Trendlines Group Receives an $8 Million Investment

2.9 NYU Tandon Future Labs Launches International Partnership with Arieli Capital

2.10 Personetics Opens New R&D Center in Nazareth to Support Continued Growth

2.11 vCita Raises $15 Million

3: REGIONAL PRIVATE SECTOR NEWS

3.1 Jordan- Oasis500 Launches Second Investment Fund to Support Young Entrepreneurs

3.2 Royal Jordanian & Private Hospitals Association Sign Agreement for Medical Tourism

3.3 CODED Raises $1.3 Million Pre-Series A Funding to Teach the Arab World Coding

3.4 Rimini Street Announces Dubai Office to Support Growing Client Base

3.5 AlgoDriven Raises $625,000 in Pre-Series A Funding from a Consortium of VC Firms

3.6 Techstars Announces Accelerator in Abu Dhabi, Second Accelerator in UAE

3.7 China’s Didi Chuxing Partners with Middle Eastern Investment Institutions to Expand in MENA

3.8 Buffalo Wings & Rings Opens Its Third Restaurant in Jeddah

3.9 Cairo Angels Announce Investment in Egyptian Mobile Gaming Company Cryptyd

3.10 COLNN Closes a Seed Round of $100,000 from EdVentures

3.11 Morocco’s Platinum Power and China’s CFHEC to Build $300 Million Hydropower Project

3.12 HSEVEN Accelerate World-Class African Startups

4: CLEAN TECH & ENVIRONMENTAL DEVELOPMENTS

4.1 Eco Wave Power Raises $13.6 Million in Stockholm IPO

4.2 Negev Ecology to Boost Waste Recycling in Southern Israel

4.3 Morocco’s ONEE to Invest MAD 51.6 Billion by 2023 Towards Water and Electricity Projects

5: ARAB STATE DEVELOPMENTS

5.1 State of the Lebanese Economy at the First Half of 2019

5.2 Lebanon’s Fiscal Deficit Falls to $73 Million in January 2019

5.3 Tourist Entries Into Lebanon Rise by 8.3% in First Half of 2019

5.4 Jordan’s Tourism Revenue Stood at $2.6 Billion for First Half of 2019

5.5 USAID Committed to Jordan’s Water Sector Amid Increases in Floods & Droughts

5.6 Baghdad Approves Iraq-Jordan Pipeline and Offshore Oil Exporting Facilities

5.7 Jordan Moves Up in the Global Cybersecurity Index Ranking

5.8 Jordanian Exports to US Worth $1.76 Billion in 2018

5.9 World Bank to Lend Iraq $200 Million for Electricity Improvement

5.10 Iran, Iraq & Syria to Create Transport Corridor

![♦]()

![♦]() Arabian Gulf

Arabian Gulf

5.11 Bahrain’s GFH Acquires $100 Million US Tech Office Portfolio

5.12 UAE & China Sign Agreements to Promote New Trade Opportunities

5.13 UAE Fund Signs $100 Million Deal to Boost Ethiopian Innovation & Entrepreneurs

5.14 Oman’s Latest Budget Update Reveals Deficit Narrowing

5.15 IMF Urges Oman to Introduce VAT as Soon as Possible

5.16 Saudi Arabia Raises Price of Petrol

![♦]()

![♦]() North Africa

North Africa

5.17 Egypt’s Inflation Rate Drops for the First Time in 2019

5.18 Egypt’s Trade Balance Deficit Hits $3.87 Billion in April 2019

5.19 Initial Surplus in Egypt’s Budget is EGP 58.2 Billion Over 11 Months

5.20 World Bank Says Egypt’s Economic Reforms are Improving Business Climate

5.21 Egypt to Hold First Exhibition for Traffic & Transport Solutions in November

5.22 World Bank Grants Loans Worth $175 Million to Tunisia for Digital Transformation

5.23 Morocco Launches MAD 1.65 Billion Home-Appliance Ecosystem

6: TURKISH, CYPRIOT & GREEK DEVELOPMENTS

6.1 Turkey Calls on US to Reverse Decision on F-35 Exclusion

6.2 Turkey to See Over 10% Growth in Tourists & Income in 2019

6.3 EU Imposes Sanctions on Turkey over Illegal Drilling in Cypriot Territorial Waters

6.4 Turkey’s Unemployment Rate Falls to 13% in April

6.5 Turkey’s Net International Investment Position Improved in May

6.6 Cyprus Has Low Labor Costs, But Low Productivity

6.7 Mitsotakis’ Top Priorities Are to Ease the Tax Burden and Create Jobs

6.8 Greek Corporate Tax Set to Drop by Almost a Third

6.9 Greece’s Growth Expected to Recover in the Second Half of the Year

7: GENERAL NEWS AND INTEREST

7.1 Obesity in Jordan Rose by 300,000 in Four Years

7.2 Egypt’s Population Reaches 99 Million

7.3 Egypt’s Cabinet Expects National Population Growth Rate to Halve Before 2052

7.4 Turkish Private University Tuition Fees Increased by 20% Annually

7.5 Greece’s Eternal Students Will Have to Graduate or Drop Out

8: ISRAEL LIFE SCIENCE NEWS

8.1 Lavie Bio Positive 2nd Year Field Results in its Bio-Stimulant Program for Wheat

8.2 Healthy.io’s Smartphone-Based Easy-to-Use Urinalysis for Women in Prenatal Care

8.3 Teva Announces FDA Approval of AirDuo Digihaler Inhalation Powder

8.4 Filterlex Medical Raised $3 Million in Series A Financing

8.5 Evogene Amends Agreement with Bayer to Include Genome Editing Targets

8.6 Equinom Cultivation Upscales Non-GMO Soy

8.7 Chardan Healthcare Acquisition Corp. Announces Merger Agreement with BiomX

8.8 Eybna Technologies Unlock the Medicinal Wonders of Cannabis

8.9 Ben-Gurion University Forensic Blood Detection Test Using Luminescence-Based Detection

8.10 StePac Takes Broccoli Packaging Out of the Ice Age

8.11 RSIP Vision’s AI Technology Provides Unmatched Precision for Lung Procedures

9: ISRAEL PRODUCT & TECHNOLOGY NEWS

9.1 SayVU Pinpoints People in Buildings with No Cellular Signal for Emergency Rescue

9.2 Arilou Automotive Cyber-Security Earns 2019 Best Practices Award by Frost & Sullivan

9.3 Get SAT Introduces Nano SAT-H for Military On-the-Move Applications

9.4 Friendly Technologies Launches WiFi Optimization & WiFi Mesh Management System

9.5 Unveiling Version 4.0 of the enSilo Endpoint Security Platform

9.6 Karamba & Alpine Electronics’ Self-Protected In-vehicle Infotainment Systems

9.7 Celeno Announces New Innovation: Wi-Fi Doppler Imaging

9.8 MSV Life Selects Sapiens’ Solutions for Its Digital Transformation Project

9.9 Credorax Partners With Cisco to Boost Payments Gateway to the Next Level

9.10 IXDen IoT Security Protection Solution for Smart Home Devices

9.11 National Utility Provider Selects Safe-T’s Innovative SDP Solution

9.12 Foresight Receives Order of QuadSight Prototype from Japan

9.13 SecuredTouch Granted Patent for Continuous User Authentication

10: ISRAEL ECONOMIC STATISTICS

10.1 Israel’s Inflation Rate Falls by 0.6% in June

10.2 Israel’s First Quarter Growth Rate is Revised Upwards

10.3 Composite State of the Economy Index for June Increases by 0.2%

11: IN DEPTH

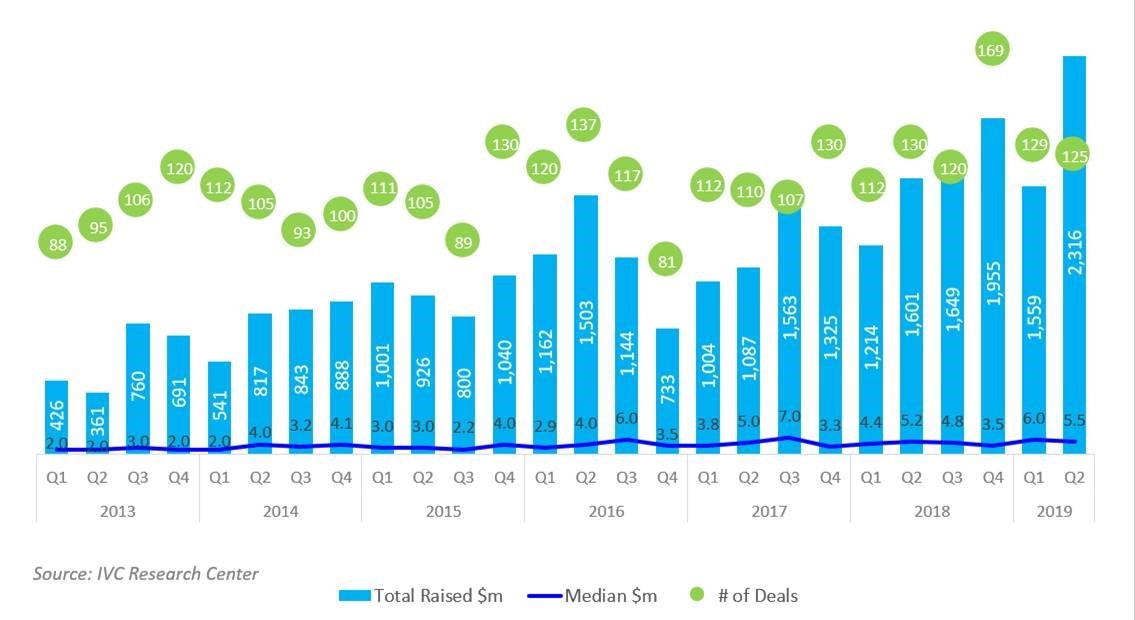

11.1 ISRAEL: Summary of Israeli High-Tech Company Capital Raising – Q2/19

11.2 ISRAEL: Israel’s Foreign Trade in Goods, by Country, as of June 2019

11.3 ARAB MIDDLE EAST: Local Startup Ecosystem is on the Rise!

11.4 IRAQ: Iraq Plans to Launch Pipelines to Export Oil Via Jordan & Syria

11.5 IRAQ: Iraqi Kurdistan’s New Government

11.6 UAE: China Deepens Ties with UAE with Industrial Investment

11.7 UAE: Moody’s Changes Sharjah’s Rating Outlook to Negative, Affirms A3 Rating

11.8 OMAN: Fiscal & Security Pressures Highlight Oman’s Unique Position in the Region

11.9 OMAN: Fitch Affirms Oman at ‘BB+’; Outlook Stable

11.10 SAUDI ARABIA: IMF Executive Board Concludes 2019 Article IV Consultation

11.11 EGYPT: Egypt Weighs Pros and Cons of IMF Loan

11.12 EGYPT: Settlement Agreement Ends Egypt’s Long-Simmering Gas Dispute with Israel

11.13 TUNISIA: IMF Staff Concludes Visit to Tunisia

11.14 MOROCCO: IMF Executive Board Concludes 2019 Article IV Consultation with Morocco

11.15 TURKEY: Fitch Downgrades Turkey to ‘BB-‘; Outlook Negative

11.16 TURKEY: EU Cuts Diplomatic Ties and Funding with Turkey Over Gas Drilling Near Cyprus

1: ISRAEL GOVERNMENT ACTIONS & STATEMENTS

1.1 Israel Launches Cybersecurity Program for Students with Communications Disorders

On 21 July, Israel launched the first cohort of a new cybersecurity training program for students with special needs. Instructed and funded by the National Cyber Security Authority and the Ministry of Labor and Social Affairs, the 250-hour program centers around the field of information security operations center (SOC). Students will receive mentorship from employees at companies including IBM and Facebook. The first cohort is made up of 16 students, all of which have varying degrees of autism and are aged 21 and older. (Calcalist 23.07)

Back to Table of Contents

1.2 Tel Aviv Residents Appeal to Municipality to Require Permits for Airbnb Operators

Twelve Tel Aviv residents have filed a petition to a Tel Aviv district court against the city and its mayor, Ron Huldai. In the petition, the plaintiffs demanded that the court compel the city to require all professional Airbnb operators to get a business license, as well as a nonconforming use permit. The plaintiffs also asked that Mayor Huldai and the city take legal action against anyone who runs a short-term apartment renting business without these two licenses.

According to the petition, the plaintiffs all own apartments and live in buildings where apartments are being used permanently as short-term rentals. Around 9,600 apartments in Tel Aviv are currently being rented out via Airbnb, the plaintiffs stated, most of them in the city’s most central neighborhoods. Though designated as residential spaces, they are being operated as a permanent business without the required permits, inconveniencing city residents and damaging the atmosphere in the neighborhoods, they added. Among the disturbances the plaintiffs named are noise nuisance in unreasonable hours due to parties; sanitation problems due to short-term tenants throwing trash in common areas, clogging the sewage systems, and causing damage to communal property; and excessive use of alcohol or illegal drugs. Such businesses also negatively affect the valuation of apartments located in the same buildings, they said.

As a result of the steep increase in the number of apartments being converted into short-term rental businesses and the damage subsequently caused to the quality of life of residents, as well as the prices being driven up in the local real estate market, the city has decided to raise the municipal tax for all such apartments. While the city has already approved the new rate for 2019 and 2020, it has yet to be approved by the Minister of Finance and the Ministry of Interior. As the Tel Aviv municipality only received the petition on 22 July, it has yet to study the claims and will respond to them in court. (Calcalist 23.07)

Back to Table of Contents

1.3 Verkhovna Rada Ratifies Free Trade Agreement Between Ukraine and Israel

The Verkhovna Rada, the Ukrainian unicameral parliament, has ratified the international agreement on free trade between the Cabinet of Ministers of Ukraine and the Government of the State of Israel. Some 230 lawmakers voted for corresponding bill No. 0223 at a plenary session of parliament on 11 July. At least 226 votes were required to pass the bill. The ratified agreement will liberalize trade in goods between Ukraine and the State of Israel. Its adoption will contribute to the further development of bilateral trade and economic cooperation between the countries, allow Ukrainian producers to benefit from the liberalization of Israel’s goods market, open up opportunities for Ukrainian businessmen to expand markets and to develop and modernize their own production. (Interfax 11.07)

Back to Table of Contents

2: ISRAEL MARKET & BUSINESS NEWS

2.1 Israeli Defense Companies Team with Lockheed Martin to Enter the US Market

Israeli defense firms have teamed up with US defense giant Lockheed Martin to market advanced military technology to the American military market. The partnerships give the Israeli companies access to US military tenders. Israel’s Rafael Advanced Defense Systems recently announced that it had signed a teaming agreement with Lockheed Martin to jointly develop, market, manufacture and support the company’s SPICE guidance kits for air-to-ground bombs.

Rafael has struck previous agreements with Raytheon for the joint marketing of its famous Iron Dome air-defense system, which has intercepted over 2,000 incoming rockets fired at Israeli population centers from the Gaza Strip since its rollout in 2011. The US Army is purchasing Iron Dome batteries.

Elta Systems, a subsidiary of Israel Aerospace Industries, has successfully completed a demonstration together with Lockheed Martin of a radar solution for the US Army’s Patriot missile-defense system. The demonstration was held as part of the US Army’s Lower Tier Air and Missile Defense Sensor program and has seen companies compete for a contract to provide radars. The demonstration, held at White Sands Missile Range in New Mexico, used a well-known Elta radar, which is also used by Rafael’s Iron Dome.

The sources said the demonstrations in New Mexico, dubbed by some local media as the “radar Olympics,” took place over a two-week period. Elta and Lockheed are competing jointly against Raytheon and Northrop Grumman for the contract. Both Elta and Lockheed Martin have produced several new-generation radars in recent years and that both bring “mature technology” to the US Army’s requirements. (IH 11.07)

Back to Table of Contents

2.2 YL Ventures Closes Fourth Fund with $120M of Committed Capital

YL Ventures has closed its fourth fund with $120 million of committed capital. YLV IV was significantly oversubscribed, and closed with a combination of current YLV investors and select new ones. Fund IV brings the total capital under YLV management to $260 million.

The YLV IV strategy will be consistent with that of previous funds, aiming to build a concentrated portfolio of top-tier seed stage cybersecurity companies out of Israel. Generally investing in only 2-3 teams each year, YLV IV will target a total of 10 companies, allowing the firm to maintain its dedication to true value-add investing. YL Ventures leads seed investment rounds with multimillion checks, while continuing to invest throughout follow-on rounds, which are typically led by top U.S. investors, including Bessemer Venture Partners, U.S. Venture Partners, ICONIQ Capital and TenEleven Ventures.

YL Ventures’ focus on cybersecurity allows it to conduct a rapidly efficient evaluation process, while supporting each of its companies, both strategically and tactically, across a number of functions post-investment. The firm is uniquely focused on supporting early stage companies’ U.S. go-to-market by leveraging its vast network of industry experts, hundreds of Chief Information Security Officers (CISOs) and U.S.-based technology companies which are prospective customers and acquirers of its portfolio businesses.

YL Ventures funds and supports brilliant Israeli tech entrepreneurs from seed to lead. With headquarters in Silicon Valley and Tel Aviv, YL Ventures manages $260 million and specializes in cybersecurity. YL Ventures accelerates the evolution of portfolio companies via strategic advice and U.S.-based operational execution, leveraging a powerful network of CISOs and global industry leaders. (YL Ventures 10.07)

Back to Table of Contents

2.3 enSilo Raises $23 Million in Series B Funding

enSilo announced a $23 million Series B funding round and significant revenue growth. The company’s latest funding round, which brings the total raised to date to over $57 million, was led by Rembrandt Ventures. The money will be used to enhance its product, drive sales and marketing initiatives, and accelerate hiring and growth across the US, Israel and other locations. enSilo also announced that it has experienced over 250% year-over-year revenue growth.

Herzliya’s enSilo‘s platform is designed to help organizations protect their endpoints and prevent data breaches. It includes next-generation antivirus, application communication control, threat hunting, detection and response, and virtual patching capabilities. (enSilo 11.07)

Back to Table of Contents

2.4 Juganu Raises $23 Million led by Viola Growth

Juganu announced the completion of a financing round, led by Viola Growth, totaling about $23 million. Additional investors participating in this financing round include OurCrowd and a Mexican investment fund.

Based on an innovative LED lighting technology capable of changing light composition and featuring an advanced infrastructure for AI technology, Juganu has developed its patented, proprietary “Digital World” technology in cooperation with software and hardware technology market leaders. One of Juganu’s closest strategic collaborations over the past five years has been with Qualcomm. This cooperation, using unique hardware developed by Juganu, allows for the “Digital World” solution to be embedded in cities and public spaces, transforming any space into an IT enterprise infrastructure with full IoT connectivity. As a result, it can serve apps and applications, such as AI, urban support for smart cars, traffic control, advanced security and rescue applications, modern municipal services, and full real-time monitoring of infrastructure

Through novel technology and smart engineering, Rosh HaAyin’s Juganu has brought to market the JLED lighting products, proving unmatched energy efficiency and long lasting lighting quality, at a competitive price. Juganu’s products are deployed worldwide for a variety of professional JLED lighting implementations such as streets and roads, gas stations, retail, office space and industrial plants. JLED cutting edge lighting systems are highly adaptable to unique and complex lighting environments, and provide unmatched energy savings and reduced maintenance costs. Juganu’s JLED lighting systems create bright and delightful experiences, improve quality of life, and build a sustainable future for people and cities around the world. (Juganu 16.07)

Back to Table of Contents

2.5 Eyesight Partnering With Leading Tier 1 to Continue Leadership in Chinese Market

Eyesight Technologies announced a partnership with a well known, publicly-traded Chinese Tier 1 to bring DriverSense, Eyesight’s Driver Monitoring System, to Automakers in the Chinese market. China is the largest auto manufacturer in the world with nearly 28 million vehicles rolling off their assembly lines last year, and with that, intelligent vehicle technologies have become a main focus. With offices in China and strong local presence, Eyesight is already providing an Aftermarket DMS solution for fleets and is now strengthening its hold on the OEM, Tier 1 market.

Based in Herzliya Pituah, Eyesight creates advanced edge-based Computer Vision and AI solutions that improve daily life experiences in the car, home, and with other consumer electronics. The company’s technology uses proprietary algorithms to deliver a range of applications, from user recognition and gaze tracking to active interactions using touch-free gesture control. With Eyesight’s technology devices both “see” and “understand” their users, unlocking a world of enhanced user experiences. (Eyesight Technologies 16.07)

Back to Table of Contents

2.6 Israel Enters Top 10 Most Innovative Nations in UN’s WIPO Index

For the first time, Israel has been ranked in the top 10 on the UN World Intellectual Property Organization’s Global Innovation Index for 2019.

For the past few years, Israel has been climbing on the UN index. In 2016, it was ranked 21st in innovation. In 2017, it jumped to 17th. In 2018, Israel placed just outside the top 10 and was ranked 11th. Israel’s precise place in the top 10 on the 2019 Global Innovation Index will be unveiled on 24 July at a special event the WIPO will be hosting in New Delhi.

The Global Innovation Index uses 80 indicators to rank the state of innovation in 129 countries. The indicators examine, among other things, the creative and supportive environment for innovation in different countries in terms of education, investment in infrastructure, investment in research, the level of business sophistication, and the political climate. The GII has become a tool used by decision-makers and business people in creating ties between the public and private sectors. The index was developed by the WIPO, Cornell University and INSEAD, one of the world’s leading business schools. (Israel Hayom 19.07)

Back to Table of Contents

2.7 UVeye Raises $31 Million from Volvo Cars, Toyota Tsusho and W.R. Berkley

UVeye announced that it has raised an additional $31M in funding, led by Toyota Tsusho, Volvo Cars and W. R. Berkley Corporation with participation of other partners like F.I.T. ventures.

UVeye’s technology enables vehicle manufacturers, logistic operators, retailers and rental car companies to carry out automatic vehicle inspection leveraging first-of-its-kind artificial intelligence, purpose-built for vehicles. Importantly, UVeye’s system has proven it can drive higher accuracy and improve efficiency, all with minimal human intervention. UVeye’s drive-through systems can detect external and mechanical flaws and identify anomalies, modifications or foreign objects – both along the undercarriage and around the exterior of the vehicle. The scanning process completes within a matter of seconds and can be used throughout the entire lifecycle of the vehicle. The technology is being actively deployed today across many use cases, from the vehicle manufacturing line – the moment components are placed on the conveyor belt through end-of-line inspection – to logistics, maintenance and beyond. Since inception UVeye has generated millions of vehicle scans across dozens of countries globally. UVeye’s Anomaly detection accuracy rate has exceeded client threshold in all case studies to date.

Volvo Cars and Toyota Tsusho intend to use UVEYE’s inspection systems at various sites internationally, including Volvo Cars’ factories dealerships and in the after-market. For Toyota Tusho, UVEYE will also support distribution to used car centers, and throughout the company’s footprint within the Japanese auto market. UVEYE welcomes these new relationships, adding to existing partnerships with Skoda and Daimler.

Tel Aviv’s UVEYE’s technology was initially developed for and deployed within the security industry, in order to detect dangerous conditions like weapons, explosives, or other threats. Upon successful deployment within some of the highest-security locations globally, UVEYE saw the opportunity to use its technology to solve challenges within the automotive industry to detect potentially hazardous mechanical issues. Today UVEYE’s suite of products includes its original undercarriage application (Helios), its revolutionary 360 solution (Atlas), and its targeted tire application (Artemis). (UVeye 22.07)

Back to Table of Contents

2.8 The Trendlines Group Receives an $8 Million Investment

The Trendlines Group has signed a Subscription Agreement with Librae Holdings Limited for a SGD10.88 million ($8 million) investment. Trendlines’ history of developing early-stage companies, combined with its hands-on investment policy and the potential of its 53 portfolio companies, makes it an attractive investment with significant potential. LH believes in Trendlines’ business model and are convinced that this represents a great opportunity. LH has been looking at Singapore as a target for a long time and views Trendlines as an avenue into that important market.

LH will purchase 103.6 million new ordinary shares in the capital of Trendlines, representing about 14.55% of the enlarged share capital of Trendlines following the placement. LH will purchase the shares at a price of SGD0.105 per share and for total consideration of SGD10.88 million ($8 million at the exchange rate of $1.00 = SGD1.360).

Misgav’s Trendlines is an innovation commercialization company that invents, discovers, invests in, and incubates innovation-based medical and agricultural technologies to fulfill its mission to improve the human condition. As intensely hands-on investors, Trendlines is involved in all aspects of its portfolio companies from technology development to business building. (The Trendlines Group 22.07)

Back to Table of Contents

2.9 NYU Tandon Future Labs Launches International Partnership with Arieli Capital

The NYU Tandon School of Engineering Future Labs — the first network of startup business hubs launched with New York City support – and Arieli Capital, a US holding company, announced a partnership to provide opportunities for investment, guidance, and networking to the Future Labs’ portfolio companies and Israeli entrepreneurs. New York City and Israel have thriving startup communities; this partnership will leverage the respective strengths to support further innovation.

The collaboration will identify promising early-stage startups through Future Labs Flash Pitch events, in which startups from New York and Israel will compete to receive an investment from Arieli Capital and its associated partners.

Ten Israeli startups will also be selected to join the Future Labs’ incubation programs. These startups will relocate to NYC and get access to the Future Labs’ full spectrum of support services, mentorship opportunities, and other resources. In the spirit of building business bridges, Arieli Capital will offer the Future Labs’ New York-based startups and program graduates a pathway to enter the Tel Aviv market through its Israel-based programs and/or associated programs.

The Arieli-Tandon partnership was initiated by Cliff Friedman, an alumnus of NYU, Chairman and CEO of ShareNett, a members-only, global network of Family Offices and professional investors who collaborate on curated, high quality alternative investment opportunities across multiple asset classes. (NYU 22.07)

Back to Table of Contents

2.10 Personetics Opens New R&D Center in Nazareth to Support Continued Growth

Personetics announced the opening of a new Research and Development (R&D) center in Nazareth, Israel. The new R&D center will support Personetics’ continued rapid growth. While the company’s R&D team has more than doubled in size in the last two years, further growth is required to support the company’s expanding customer base, which now includes more than 30 of the world’s leading banks, as well as new solutions the company is bringing to the market including the recently announced small business and banker enablement solutions.

While the shortage of skilled programmers is a global phenomenon, increasing the diversity of the R&D pool both geographically and demographically is critical to the future growth of advanced technology companies. Establishing a center in Nazareth allows the company to tap into a hotbed of highly skilled professionals, enabling expansion of R&D capabilities while maintaining proximity to facilitate close collaboration. Being in the same time zone and less than a two-hour drive away is a big advantage for their teams in Tel Aviv and Nazareth.

The opening of Personetics’ Nazareth office was aided by the Tsofen organization, which works to integrate skilled Arab workers into the Israeli high-tech industry and bring high-tech companies to Arab cities. Since Tsofen’s establishment, the number of high-tech companies operating in Nazareth has jumped from one to forty.

Tel Aviv’s Personetics is the leading provider of customer-facing AI solution for financial services and the company behind the industry’s first Self-Driving Finance![™]() platform. Harnessing the power of AI, Personetics’ Self-Driving Finance solutions are used by the world’s largest financial institutions to transform digital banking into the center of the customer’s financial life – providing real-time personalized insight and advice, automating financial decisions, and simplifying day-to-day money management. (Personetics 22.07)

platform. Harnessing the power of AI, Personetics’ Self-Driving Finance solutions are used by the world’s largest financial institutions to transform digital banking into the center of the customer’s financial life – providing real-time personalized insight and advice, automating financial decisions, and simplifying day-to-day money management. (Personetics 22.07)

Back to Table of Contents

2.11 vCita Raises $15 Million

vCita announced that it completed a $15 million financing round led by Forestay Capital. The Herzliya-based startup previously raised $15 million from private Israeli investors. With 90 employees, most of them in Israel, the company was founded in 2010. The financing will be used to increase the rate of growth and invest mainly in technology and marketing, and to invest in creating strategic partnerships. The company is planning to double its number of employees within 12 to 18 months and that revenue has doubled over the past year to several tens of millions of dollars annually. vCita has about 100,000 paying customers.

Tel Aviv’s vCita is the #1 business management and client engagement app, designed to help small businesses grow. Tailored specifically for service providers, vCita redefines the way businesses interact with their clients, driving more opportunities from the web, mobile, email and social while empowering clients to self-serve. vCita includes an online CRM to manage all client communications together with online scheduling, online payments, email & SMS campaigns, lead generating website widgets, and everything a small business needs to drive more business and provide great client service. (vCita 22.07)

Back to Table of Contents

3: REGIONAL PRIVATE SECTOR NEWS

3.1 Jordan- Oasis500 Launches Second Investment Fund to Support Young Entrepreneurs

Oasis500 announced the launch of a second fund with support from the King Abdullah Fund for Development (KAFD), the Innovative Start-ups and SMEs Fund (ISSF) and the Arab Bank. The second Oasis fund aims to drive social and economic change by investing up to $100,000 in effective entrepreneurs to establish ICT and innovative industrial companies. The investment includes a six-month business acceleration program, and a program offering technical supervision and guidance services from ‘high-level’ councilors, among other services. The program will conclude with entrepreneurs showing their projects to investors and partners in order to receive post finance and help their companies grow, the statement said.

Amman’s Oasis500 is a pre-seed and seed fund manager and accelerator that catalyzed the development of an entrepreneurial ecosystem in the region, continues to create opportunities for aspiring entrepreneurs and enables them to build their own companies that subsequently contribute to the local economy. Since inception in 2010 by direction from King Abdullah II, Oasis500 has invested $8.65 Million in 154 technology and creative startups, that were able to raise over $60 Million from third party investors. (Oasis500 15.07)

Back to Table of Contents

3.2 Royal Jordanian & Private Hospitals Association Sign Agreement for Medical Tourism

On 16 July, Royal Jordanian and the Private Hospitals Association (PHA) signed a cooperation agreement aimed at supporting and promoting medical tourism to the Hashemite Kingdom and strengthening Jordan’s position as a destination for treatment and hospitalization for citizens from various countries in the region. Under the accord, RJ will provide discounted tickets on business and economy classes to Arab and international patients, and their companions, who come to Jordan to receive medical treatment at medical centers and hospitals that are members in the association.

The PHA will cooperate with Royal Jordanian toward bringing a greater number of incoming patients from abroad to be treated in Jordan. RJ, Jordan’s national carrier, took the initiative to facilitate air travel for Arab and foreign patients on its route network through discounts such as those involved in this agreement. The agreement is viewed as an investment opportunity that will both serve the private hospitals and stimulate travel on RJ aircraft, supporting, in turn, the national economy. (Petra 16.07)

Back to Table of Contents

3.3 CODED Raises $1.3 Million Pre-Series A Funding to Teach the Arab World Coding

CODED, the Kuwait based coding academy, has secured a Pre-Series A funding of $1.3 million led by KISP. Other participants in the funding round included 500 startups, Sijam Ventures, Sirdab Lab, Sharq Capital and Abdullah Al-Zabin. CODED started in 2015, aiming to teach coding in Arabic to the enthusiastic Arab youth, both online and offline. In 2017, the Kuwaiti startup launched Barmej Online Boot Camps, with an objective to reach out to every Arab who wants to learn coding. With the online platform, the boot camp participants can get hands on experience in coding with practical learning projects that are reviewed by expert trainers. With a flexible learning experience and top notch educational material, the boot camps help the participants prepare for high quality job placements.

CODED hopes to add more Barmej Boot Camps with its newly-secured investment. By developing the platform even further, the educational platform wants to place its graduates in different jobs in various fields of coding technology.

CODED previously raised an undisclosed SEED round in early 2017, which helped them develop Barmej at early stage. Currently Barmej learning has over 200,000 users on 8 different free learning tracks spanning different programming languages and technologies. With their large pool of students, the CODED has become a partner of the 1 Million Arab Coders Program. It has also been selected as one of the top 100 startups in the Arab World by the World Economic Forum. So far the offline boot camps of Barmej has seen over 250 graduated coders. (CODED 23.07)

Back to Table of Contents

3.4 Rimini Street Announces Dubai Office to Support Growing Client Base

Las Vegas, Nevada’s Rimini Street, a global provider of enterprise software products and services, announced it is significantly strengthening its investment in and commitment to the Middle East by establishing Rimini Street FZ–LLC, opening a new office in Dubai and hiring local staff. The Company’s increased investment is in response to its growing client base with operations in the Middle East and accelerating local demand for its portfolio of award-winning, ultra-responsive enterprise software support services.

Rimini Street has been present in the Middle East for over five years supporting nearly 100 organizations with operations in the region, including clients in the Arabian Gulf and Saudi Arabia. Rimini Street plans to add staff to market, sell and service clients in local language. The new Dubai office will provide clients with more comprehensive support services compared to standard vendor maintenance including support for customizations, interoperability and performance tuning. (Rimini Street 10.07)

Back to Table of Contents

3.5 AlgoDriven Raises $625,000 in Pre-Series A Funding from a Consortium of VC Firms

Dubai’s AlgoDriven has successfully raised $625,000 in fundraising from a consortium of both domestic and international venture capital firms. Joining the round are regional investors, Oman Technology Fund and DTEC Ventures. International venture capital firms include 500 Startups through their MENA based 500 Falcon’s Fund, as well as Silicon Valley based Social Capital. This new investment will enable AlgoDriven to further capitalize on its position as a market leader in automotive data and software field, in the Middle East, and internationally in Australia and New Zealand. New product innovation is a key focus of AlgoDriven, which will help car dealers, banks and insurance companies evaluate used cars more accurately. International expansion is also a key focus over the coming months, as AlgoDriven pushes into the wider MENA market and beyond. (MAGNiTT 14.07)

Back to Table of Contents

3.6 Techstars Announces Accelerator in Abu Dhabi, Second Accelerator in UAE

Boulder, Colorado’s Techstars announced the launch of the Techstars Hub71 Accelerator. In partnership with Hub71, an Abu Dhabi-based global technology hub led by Mubadala Investment Company, the new 13-week mentorship-driven accelerator will provide hands-on mentorship and guidance as well as access to Techstars’ worldwide network, to help startups gain traction and accelerate their businesses for global success. The Techstars Hub71 Accelerator will be based at Hub71 in Abu Dhabi. The Techstars Hub71 Accelerator will accept 10 startups on an annual basis and is open to startups addressing technology innovations across a variety of business verticals.

Techstars is the worldwide network that helps entrepreneurs succeed. Techstars founders connect with other entrepreneurs, experts, mentors, alumni, investors, community leaders, and corporations to grow their companies. Techstars operates three divisions: Techstars Startup Programs, Techstars Mentorship-Driven Accelerator Programs and Techstars Corporate Innovation Partnerships.

Hub71 is a global ecosystem in Abu Dhabi offering an interconnected network to enable innovation and growth opportunities for transformational tech companies and startups, creating an environment where entrepreneurs can thrive. It is a flagship initiative of the ‘Ghadan 21’ program working to accelerate Abu Dhabi’s economy. Alongside strategic partners Microsoft, SoftBank Vision Fund, Abu Dhabi Global Market and Mubadala, Hub71’s mission is to create an optimal environment for outstanding innovation making economic and social impact. (Techstars 23.07)

Back to Table of Contents

3.7 China’s Didi Chuxing Partners with Middle Eastern Investment Institutions to Expand in MENA

Chinese unicorn Didi Chuxing has signed a strategic agreement with Symphony Investment and some other investment institutions in the Middle East. The agreement will enhance the partnership between the MENA region and China. The parties that signed the agreement will set up an Abu Dhabi based joint venture, aiming to promote internet consumer services and sharing economy in the region. Mubadala Investment Company is considering joining the consortium as well.

Symphony Investment has renowned funders such as Emaar Properties, Aramex, Americana Group and Noon. The agreement was signed at the UAE-China Economic Forum, organized by the UAE Ministry of Economy. China currently ranks second among the trading partners of the MENA region and the bilateral cooperation between the two includes finance, manufacturing, technology and commerce. (Various 23.07)

Back to Table of Contents

3.8 Buffalo Wings & Rings Opens Its Third Restaurant in Jeddah

Cincinnati’s Buffalo Wings & Rings, one of the leading American food restaurants in the region, announced the opening of its third branch in Jeddah, Saudi Arabia. The new club-level sports restaurant experience means everyone is a VIP, worthy of the ultimate sports dining experience. With bright, inviting dining rooms, 50+ TVs, elevated fan experiences, chef-inspired recipes and of course signature wings, Buffalo Wings & Rings is the ideal experience for socializing with friends & family over sports.

The Emaar square branch is conveniently located at a close proximity to malls and university in the heart of Jeddah and can accommodate over 100 guests at their indoor and outdoor seating areas. The outdoor area is conveniently facing the famous Emaar fountain and features live entertainment on weekends. In addition to the brand’s promise of maintaining the fresh flavors at a great value, this branch is decorated with a new modern and sleek look that provide customers with ambiance. (Buffalo Wings & Rings 21.07)

Back to Table of Contents

3.9 Cairo Angels Announce Investment in Egyptian Mobile Gaming Company Cryptyd

The Cairo Angels, a global network of angel investors focused on supporting startup opportunities in the MENA region, announced its most recent investment in Cryptyd. Alexandria’s Cryptyd, a mobile game development company established in 2016. The company has developed five mobile games to date; and is seeking to launch two games in the upcoming months. The new investors are affiliated with Cairo Angels and the Alexandria Angels. This is the second investment round for the company, with its seed investment raised in 2015 from The Cairo Angels.

The Cairo Angels continues to see exponential growth in the gaming industry, having invested in two gaming companies to date. The Cairo Angels is aligned with the Cryptyd team on their prospects for the market, believing that mobile gaming is currently experiencing monumental growth. The game development industry is becoming less of a niche arena, and is catering to a larger audience due to high smartphone penetration within the region. This is increasing overall industry revenue, while simultaneously increasing competition of game development companies exponentially. The industry is gaining momentum, and investment in such companies leads to higher levels of innovation, clustering of talent, and display of pure artistic abilities. (Cairo Angels 16.07)

Back to Table of Contents

3.10 COLNN Closes a Seed Round of $100,000 from EdVentures

Egypt’s EdVentures, a leading Arab world corporate venture capital fund specializing in education, culture and innovative learning solutions, has just added a new startup to its portfolio of companies. The company will invest in Giza’s COLNN, a school SaaS provider. COLNN’s services include web cloud-based solutions to schools and an integrated mobile app connecting teachers, parents, and students.

COLNN helps schools manage their internal processes, departments and activities in addition to optimizing the usage of their available resources through school management system (SMS). Upon analyzing the needs and requirements of each school, COLLN customizes their solutions/software to perfectly fit the nature and requirements of each school. Their services don’t end at the development phase; they also provide continuous training and follow-up to the schools’ staff, students and parents helping them to get maximum benefits of the newly updated learning process/system.

EdVentures invests in startups specializing in education, culture and innovative learning solutions in SEED and Pre-Series A rounds focusing on Egypt, Africa, and the Arab World. The corporate VC was launched in 2017 by Nahdet Misr Publishing House. It provides technical and financial support to startups in order to ensure success and continuity in the market by providing investment according to the needs and maturity level of each company. (MAGNiTT 14.07)

3.11 Morocco’s Platinum Power and China’s CFHEC to Build $300 Million Hydropower Project

Morocco’s Platinum Power and China’s CFHEC are set to build a $300 Million hydropower project in Morocco. Platinum Power and CFHEC will also partner on renewable energy projects elsewhere in Africa, albeit this will be the first time the companies have partnered on a project.

Platinum Power is a Morocco-based company, majority-owned by US investment fund Brookstone Partners. It specializes in the development, financing, and construction of renewable energy projects. It is a key player in the hydropower industry in Morocco. Last October, the company received authorization from the Moroccan Ministry of Energy to build eight new hydropower projects across the country. Platinum Power is also currently developing projects in Cameroon and Ivory Coast. (MWN 11.07)

Back to Table of Contents

3.12 HSEVEN Accelerate World-Class African Startups

Casablanca’s HSEVEN, Africa’s largest accelerator, is launching “HSEVEN DISRUPT AFRICA”, an ambitious startup acceleration program designed for entrepreneurs of the Moroccan and African diaspora. The 6-month program will provide a seed investment of €150,000 plus an eventual investment of €500,000 to €1.5 million. HSEVEN DISRUPT AFRICA is designed to support exceptional entrepreneurs building high-impact startups, and targets seed and early stage startups with 2 to 5 founders that are eager to impact Africa through innovative services, products and business models.

The program will start with a global call for applications, followed by an international selection roadshow in New York, Montréal, San Francisco, Shanghai, Dubai, London, Amsterdam, Paris and Casablanca. The selected startups will benefit from a seed investment of €150,000 at the beginning of the program for 5 to 7% equity, then an eventual investment of €500,000 to €1.5 million at the end of the program. These investments will be granted through a partnership with the venture capital firm Azur Partners. The program will also benefit from funding of the Dutch Good Growth Fund (DGGF) and the Innov-Invest program of the Caisse Centrale de Garantie (CCG) with the support of the World Bank. The startups will be located at HSEVEN’s 12,000 ft² campus in the heart of the Marina of Casablanca. (HSEVEN 16.07)

Back to Table of Contents

4: CLEAN TECH & ENVIRONMENTAL DEVELOPMENTS

4.1 Eco Wave Power Raises $13.6 Million in Stockholm IPO

Israeli-Swedish wave energy company Eco Wave Power has raised $13.6 million at a company value of $58 million in its IPO on the Nasdaq First North stock exchange, an exchange for growth companies that is a secondary market of the Scandinavian stock exchanges, which are owned by Nasdaq. The share price in the IPO was 19 Swedish krona. The share price dropped to 17.7 krona in the first days of trading in the share, reflecting a $54 million market cap. Some 5,900 investors participated in the offering, including investment institutions AP4 and Skania Fonder, which became the largest shareholders in Eco Wave Power following the offering.

Eco Wave Power, a renewable energy company that has developed technology for turning sea waves into electricity, has 13 employees. The company’s Israeli subsidiary was founded in 2011 in Tel Aviv. Eco Wave Power says that it is the only company in world operating a system for producing energy from waves that is connected and selling electricity to a network under a commercial agreement for purchasing electricity. The company says that the purpose of the IPO is to construct an initial commercial farm for producing energy from sea waves, and for expanding its projects and marketing and sales activity. The company reported that it currently had two energy production farms, one in Jaffa and one in Gibraltar, and that there were plans for expanding both of them. Eco Wave Power’s projects total 190 megawatts in a number of countries. (Eco Wave Power 21.07)

Back to Table of Contents

4.2 Negev Ecology to Boost Waste Recycling in Southern Israel

Recycling and waste treatment company Negev Ecology has acquired a 49% stake in the Dudaim Recycling and Environmental Education Park in southern Israel from the Bnei Shimon Regional Council Economic Corporation for NIS 47 million. Negev Ecology, headquartered in Kibbutz Mishmar HaNegev, is a leader in waste recycling and treatment. It operates 10 waste recycling facilities of various kinds all over Israel. Negev Ecology already operated the Dudaim facility, and will continue operating after acquiring 49% of it through a joint team.

Dudaim Park sorts and treats waste collected from all of southern Israel. An innovative plant will be built there at a cost of NIS 70 million that will sort and recycle half of the waste brought to the site. The new venture will substantially reduce the need to bury waste. The first sorting and recycling plant in the south will soon be built there, and will make it possible to significantly increase waste recycling in all the local authorities sending their waste to Dudaim Park. (Globes 22.07)

Back to Table of Contents

4.3 Morocco’s ONEE to Invest MAD 51.6 Billion by 2023 Towards Water and Electricity Projects

Morocco’s National Office for Electricity and Drinking Water (ONEE) presented its 2019-2023 ambitions at its board of directors meeting in Rabat. The ONEE’s strategy is designed to improve access to electricity and drinking water across Morocco. MAD 8.6 billion will go towards electricity production projects generating up to 4.262 MW. In accordance with Morocco’s renewable energy goals, 4.240 MW of this power will be generated from solar, hydroelectric and wind power. Morocco intends to produce 52% renewable energy by 2050.

In addition to the renewable projects, ONEE announced its intention to oversee the completion of the Dakhla diesel power station projects (22MW) and the Abdelmoumen pumped-storage hydroelectricity station (350 MW) by 2023. French construction company Vinci won the tender for the MAD 3 billion Abdelmoumen station in January 2018. Construction work for the project began in October last year. Finnish corporation Wartsila won the tender for the Dakhla power station project in August 2017, but construction on the project has to this date not yet commenced.

By 2023, ONEE also intends to invest MAD 8.7 billion in regional integration projects. ONEE is evaluating the feasibility of infrastructure connection projects with Mauritania and Portugal. ONEE will also invest MAD 5.2 billion towards reinforcing access to electricity in rural areas, and extend distribution of electricity to 30,900 households across Morocco.

ONEE is responsible for the delivery of drinking water across Morocco, and has pledged to invest MAD 25.5 billion to this end. MAD 15.2 million will go towards improving access to water in urban areas, including the construction of 3400 km of new water pipes. MAD 4.6 billion will go towards reinforcing water treatment, through the construction of 64 new treatment plants by 2023. ONEE will also invest MAD 5.7 billion towards improving access to drinking water in rural areas to 99.3%. The latest ONEE figures show 96.6% of households had access to safe drinking water in 2017. (MWN 22.07)

Back to Table of Contents

5: ARAB STATE DEVELOPMENTS

5.1 State of the Lebanese Economy at the First Half of 2019

BLOM Bank observed the state of the Lebanese economy at the close of the first half of 2019. The bank found that Beirut now has an opportunity to implement reforms and turn the tide. In June 2019, an IMF panel visited Lebanon and released a concluding statement assessing the overall environment. The main parameters attesting to the authorities’ path towards fiscal consolidation are: the 2019 pledge to reduce the national fiscal deficit to 7.6% of GDP (instead of 2018’s 10.9%) via a new tax-driven budget inclusive of multifaceted national reforms, as well as the endorsement of the Electricity Reform Plan by parliament in April 2019.

The authorities in 2019 took a number of eminent steps forward which earns it some points. Even though the pledged deficit figure (7.6% of GDP) is considered too ambitious and the more reasonable target stands at approx. 9% of GDP, the authorities have taken a number of steps forward (revealing a stronger commitment to fiscal adjustment) which seem to speak louder than the pledged deficit. For instance, the government froze public sector hiring for the next 3 years, set a ceiling on the allowances of public sector employees for a first in the history of the country, and approved a modernized version of the outdated law of commerce.

Nonetheless, growth was subdued in H1/19, as Lebanon’s private sector refrained from investing in future business. Lebanon’s economic growth stood at an estimated 0% in H1/19. Economic growth was capped due to sectorial slowdowns as well as persisting crowding out of the private sector in the first half of the year due to high interest rates. In fact, the BLOM Purchasing Managers’ Index (PMI), a predictive power for economic growth, stalled at an average of 46.5 in H1/19, compared to 46.6 and 47.1 in H1/18 and 2017, respectively. The average PMI score in H1/19 was underpinned by persisting pressures on private sector companies who adopted a wait-and-see approach as they monitor the political and economic reform plan to gradually materialize, stabilize the operating environment, and kick start their investment. (BLOM 13.07)

Back to Table of Contents

5.2 Lebanon’s Fiscal Deficit Falls to $73 Million in January 2019

Lebanon’s fiscal deficit (cash basis) narrowed from $378.91M in January 2018 to $72.83M in January 2019. This was attributed to a 16.1% yearly decrease in government expenditures to hit $1.10B, while the fiscal revenues recorded a yearly increase by 8.45% to stand at $1.08B. The primary balance which excludes debt service posted a surplus of $231.74M, compared to a deficit of $106.34M in January 2018. Tax revenues (constituting 83.4% of total revenues) declined by an annual 1.13% to $902.5 million in January 2019. Revenues from VAT (33.8% of total tax receipts) dropped by 16% y-o-y to $305.4 million.

Although the new VAT rate of 11% was applied in the beginning of January 2018, increasing from 10%, the decrease in the VAT revenues can be linked to the stagnating economy and recession in many sectors. In the automotive sector, the VAT payment is done after car registration. However, according to the Association of Lebanese Car Importers, the total number of newly registered commercial and passenger cars fell by 26.1% year- on- year (y-o-y) to 1,948 cars in January 2019. Meanwhile, customs’ revenues (11.79% of tax receipts) dropped by 6.49% year-on-year (y-o-y) to $106.38M. As for non-tax revenues (16.6% of total revenues), they witnessed a significant increase from 84.92M in January 2018 to $179.57M in January 2019. This can be linked to the yearly rise in telecom revenues (constituting 46.31% of total non-tax revenues) to reach $83.17M in January 2019.

On the expenditures’ side, total government spending retreated by a yearly 16.1% to hit $1.10B in January 2019. Transfers to Electricity du Liban (EDL) alone dropped by 26.17% to reach $65.85M, which followed the 12.78% annual decline in average oil prices to $60.24/barrel over the period. Moreover, total debt servicing (including the interest payments and principal repayment) reached $304.57M in January 2019, up by a yearly 11.74% such that interest payments alone rose by 12.77% y-o-y to $287.34M. Interest payments on domestic debt grew by 14.27% y-o-y to $245.51 following the increase in interest rates on treasury bills in November 2018. Meanwhile, interest payments on foreign debt rose by an annual 4.69% to $41.83M. For its part, the treasury transactions posted (includes revenues and spending that are of temporary nature) a deficit of $50.10M, compared to $59.96M in January 2018. Treasury expenses of which municipalities dropped from $274.60M to $20.08M over the same period noting that the government released overdue funding to municipalities in the following months. (MoF 11.07)

Back to Table of Contents

5.3 Tourist Entries Into Lebanon Rise by 8.3% in First Half of 2019

The recently released Ministry of Tourism report revealed an increase in the number of tourists from 853,087 by June 2018 to 923,820 by June 2019. The composition of total tourists by June 2019 showed that tourists from Europe grasped the lion’s share at 35.82%, with Arab countries coming in second with a share of 32.16%, North America with 17.75% and finally Asia with 7.47% of total tourists. The remainder share of 6.8% is split between African, Oceanic and other countries.

The number of European tourists increased by a significant 10.3% YoY amounting to 330,928, the highest historical figure for Lebanese tourism by H1/19. Most notably, visitors from Arab countries surged by 21.4% YoY, totaling 297,112 by June 2019. The number of tourists from Iraq and Egypt increased significantly by 11.00% YoY to 101,637 and 5.35% YoY to 49,462, respectively. This surge is also the result of the lifting of the Saudi travel ban on Lebanon, which explains the 90.8% rise in the number of tourists from the country which hit 44,736 tourists from the KSA alone by June 2019.

The number of African tourists declined 44.1% year-on-year to reach a figure of 29,480 visitors by June. This was compensated by the inflow of new tourists from America, Asia, Europe and Arab countries. The number of tourists from North America and Asia increased by 5.5% YoY to 163,949 and 6.4% YoY to 69,036, respectively. (Ministry of Tourism 19.07)

Back to Table of Contents

5.4 Jordan’s Tourism Revenue Stood at $2.6 Billion for First Half of 2019

Jordan’s tourism sector delivered a six-month revenue of $2.6 billion with over 2.438 million visitors arriving in the Kingdom since the beginning of the current year continuing a strong rebound that started in late 2016. The Central Bank of Jordan (CBJ) said tourism income surged by 8.3% during the January-June period of the current year at $2.6 billion against $2.4 billion for the same period of 2018. Breaking down the figures, the CBJ said June saw a major increase in both tourist revenue and arrivals soaring by 26.9 and 26.5% respectively. (Petra 15.07)

Back to Table of Contents

5.5 USAID Committed to Jordan’s Water Sector Amid Increases in Floods & Droughts

USAID’s current allocation to support Jordan’s water sector stands at around $80 million per year, according to a senior USAID official, who said that the agency is now working with the Kingdom in two main areas: source water and non-revenue water. A major priority of the agency is helping its partner countries better cope with future shocks and stresses and to build resilience.

The Jordanian Water Ministry announced in May that it had begun implementing the first government-proposed effort to minimize water waste via the non-revenue water (NRW) project. The project, first proposed during the London initiative, will cost $50 million, according to the ministry. The ministry also said at the time that preparations were under way for a project to desalinate water in the Hasban wells outside Amman, indicating that the project, in addition to a third expansion project for Al Samra Wastewater Treatment Plant, were all proposed at the London initiative 2019, which was held in February to enhance economic growth and reform in Jordan. As part of the initiative, a number of countries and institutions have pledged funds to support Jordan as it tackles the aforementioned challenges.

Jordan, categorized as the world’s second water-poorest nation, faces a set of intricate challenges which include the implementation of water and sanitation projects, the search for water sources to compensate for NRW and upgrading water infrastructure, according to experts in the field. USAID recognizes that water is a cross-cutting issue in foreign assistance and that it touches many of the development outcomes in areas including human health and dignity, environmental management, economic growth and the empowerment of women and girls. USAID Office of Water’s annual appropriation has been increasing for the past several years. In 2013 for example, it was at $315 million a year, and it has steadily increased every single year since then up to $435 million today. (JT 21.07)

Back to Table of Contents

5.6 Baghdad Approves Iraq-Jordan Pipeline and Offshore Oil Exporting Facilities

On 9 July, the Iraqi Cabinet met in Baghdad under the chairmanship of Prime Minister, Adil Abd Al-Mahdi, at which it discussed a series of recommendations by the Ministerial Committee for Energy regarding a number of strategic projects aimed at increasing Iraq’s oil production and exporting capacities. The Cabinet approved the proposed Iraq-Jordan oil pipeline, and the construction of offshore oil exporting facilities in Iraq’s territorial waters in the Arabian Gulf.

The Cabinet also approved several measures to encourage Iraqi, Arab and international investment in Iraq, including further action to cut red tape and streamline procedures. The Cabinet approved a draft law on the accession by the Republic of Iraq to the 1997 Protocol to amend the International Convention for the Prevention of Pollution from Ships (1973) as modified by the 1978 Protocol. (GoI 11.07)

Back to Table of Contents

5.7 Jordan Moves Up in the Global Cybersecurity Index Ranking

According to the Global Cybersecurity Index (GCI) for 2018, Jordan has moved up 18 spots on the global ranking and two spots on the regional ranking. Globally, Jordan moved up from 92nd place to 74th and from 10th place to 8th place among Arab countries, according to the report, which was conducted by the UN’s International Telecommunication Union (ITU) to review the cybersecurity commitment of each UN member state.

The Kingdom has witnessed remarkable improvement in cybersecurity development according to the GCI, almost doubling its score from 2017 to 2018. The Ministry of Digital Economy and Entrepreneurship has said that the improvement in the Kingdom’s performance was achieved by the joint efforts of the ministry, the Jordan Armed Forces-Arab Army, security bodies, the Central Bank of Jordan and the private sector.

The report, which was released earlier this month, aims at raising awareness of cyber-related issues and sharing best security practices by measuring each participating country’s preparedness to prevent cyber threats and manage and control cyber incidents. The GCI evaluates each country’s cybersecurity on the basis of five pillars: legal, technical, organizational, capacity building and cooperation.

Jordan’s cyber environment is mature, the report indicated, as a result of the Kingdom’s National Cybersecurity Strategy and National Computer Emergency Response Team (JO-CERT), along with its operating fiber-optic network. The government has conducted several technical activities related to protecting citizens’ cybersecurity, including providing the National Broadband Network (optical fiber connection between all government entities) with an additional layer of security, according to the ITU website.

In addition, to manage and harmonize approaches to cyber risks and threats among all government entities, the government established JO-CERT. Jordan has also conducted national electronic authentication projects by adopting a public key infrastructure solution, the report added — a project that includes a smart ID project to replace traditional IDs with smart identification cards. (JT 19.07)

Back to Table of Contents

5.8 Jordanian Exports to US Worth $1.76 Billion in 2018

The 8th session of the Joint Jordanian-American Committee concluded on 15 July, during which the committee discussed bilateral economic cooperation in various fields and means of enhancing trade exchange between the two countries. The committee, chaired by the Secretary-General of the Ministry of Industry, Trade and Supply, Yousef Al Shamali and the US representative Daniel Melani, also reviewed mechanisms of joint cooperation that reflected positively on trade between the two countries in light of the Free Trade Agreement signed between them in 2001.

The volume of Jordanian exports to the US, which reached $1.76 billion in 2018, focused mainly on knitted and manufactured garment, while imports amounted to $1.77 billion. Machinery, fuel derivatives, electrical appliances, wheat and pharmaceuticals are the main goods imported by the Jordanian market from the US. The Jordanian government thanked the American side for its continuous support for the Kingdom in a number of sectors, namely the support provided by the US Agency for International Development (USAID) in its programs targeting the commercial and economic sectors. (Roya 15.07)

Back to Table of Contents

5.9 World Bank to Lend Iraq $200 Million for Electricity Improvement

The World Bank will reportedly lend a total of $200 million to Iraq for upgrades to its electricity grid. The agreement was signed by Iraqi Finance Minister Fuad Hussein and Yara Salim, a representative to the World Bank. Iraq is expected to implement the projects within five years, and repay the debts in ten to 15 years. (Basnews 10.07)

Back to Table of Contents

5.10 Iran, Iraq & Syria to Create Transport Corridor

High-ranking officials from Iran, Syria, and Iraq have agreed to create “a multimodal transport corridor” a part of efforts to boost trade relations between the three nations. The railroad project connecting Iran’s Shalamcheh to Iraq’s Basra will be accelerated so that the two countries’ rail networks are connected to each other and then connected to Syria.

During Iranian President Hassan Rouhani’s visit to Iraq in March, the two countries signed five deals to promote cooperation in various fields. The documents entail cooperation between Iran and Iraq concerning the Basra-Shalamcheh railroad project, visa facilitation for investors, cooperation in the health sector, and agreements between the Ministry of Industry, Mines and Trade of Iran and Ministry of Trade of Iraq, and another one in the field of oil between the petroleum ministries of the two countries. Iran’s Minister of Industry, Mine and Trade Reza Rahmani has said that Tehran and Baghdad have agreed to reach the target of raising the value of annual trade exchange to $20 billion within two years. (Tasnim 07.07)

Back to Table of Contents

►►Arabian Gulf

5.11 Bahrain’s GFH Acquires $100 Million US Tech Office Portfolio

GFH Capital Limited, a subsidiary of Bahrain-based GFH Financial Group, announced that it has acquired a tech offices portfolio in the United States in a deal valued at over $100 million. The acquired portfolio consists of five income yielding buildings located in Research Triangle Park, North Carolina. The portfolio was purchased in partnership with Global Mutual, one of the fastest growing real estate investment management company in US, UK and Europe operating over £1.5 billion of assets under management. The portfolio is situated on nearly 60 acres within the Research Triangle Park, which is the largest dedicated scientific research park in the US, featuring more than 250 companies and 50,000 professionals within 22.5 million square feet of built-out space. GFH Financial Group, along with its investors, acquired about 95% of the portfolio with the remainder to be held by Global Mutual and its affiliates.

With the completion of this deal, total US and UK real estate transactions executed by GFH over the last few years has crossed $1 billion mark, the company said in a statement. (AB 16.07)

Back to Table of Contents

5.12 UAE & China Sign Agreements to Promote New Trade Opportunities

On 22 July, Sheikh Mohamed bin Zayed Al Nahyan, Crown Prince of Abu Dhabi, and Xi Jinping, President of the People’s Republic of China witnessed the signing of a number of agreements between the two countries, spanning a range of sectors. The signing of the agreements seek to further advance strategic ties between the UAE and China, opening up new partnership horizons across various fields. They cover such sectors as defense, trade and investment, environment and sustainability, education, ports & customs and energy.

They include an agreement on defense and military cooperation between the two countries, a memorandum of understanding (MoU) on environment protection and conservation and an MoU on scientific and technological cooperation, with a focus on artificial intelligence technologies. The agreements also include a deal between the UAE Office for Future Food Security and China’s Ministry of Agriculture and Rural Affairs in the Inner Mongolia Autonomous Region on two projects to ensure food security advancement, and integrated farming systems.

The two countries signed an MoU on peaceful use of nuclear energy, another to introduce the Chinese language in UAE education curricula while the Department of Culture and Tourism – Abu Dhabi signed an agreement with the National Museum of China. Abu Dhabi National Oil Company signed an agreement with China National Offshore Oil Corporation while the Abu Dhabi Global Development Market and China’s National Development and Reform Commission signed a MoU to encourage Chinese and UAE enterprises’ trade and investment opportunities. The signing ceremony also saw a MoU between Abu Dhabi Ports, Jiangsu Provincial Overseas Cooperation and Investment Company, and the Industrial and Commercial Bank of China and another between the Emirates Nuclear Energy Corporation and the China National Nuclear Corporation. A joint research cooperation agreement was also inked between Khalifa University of Science and Technology and Tsinghua University. (AB 22.07)

Back to Table of Contents

5.13 UAE Fund Signs $100 Million Deal to Boost Ethiopian Innovation & Entrepreneurs

The Abu Dhabi-based Khalifa Fund for Enterprise Development (KFED) has signed a partnership agreement with the Ethiopian Ministry of Finance aimed at providing over $100 million to help promote a culture of innovation and entrepreneurship in the African country. The new agreement will help pave the way in enhancing innovation and supporting entrepreneurs in Ethiopia. The UAE has maintained strong ties with the Federal Democratic Republic of Ethiopia after Abu Dhabi Crown Prince Sheikh Mohamed bin Zayed Al Nahyan’s visit to Addis Ababa last year.

The funding to be received as part of the agreement will enable the implementation of a series of projects that are aimed at consolidating the Ethiopian government’s efforts to create a stable and balanced economy while also driving in other benefits like the creation of employment opportunities for the youth, women empowerment and enhanced capacity building for entrepreneurs and local institutions. The allotted $100 million will be supervised and maintained by the Ministry of Innovation and Technology, in cooperation with KFED.

The Khalifa Fund for Enterprise Development, which was established 12 years ago in Abu Dhabi, supports small and medium enterprises (SMEs) in the UAE and has funded more than 1,600 projects within the UAE and across 20 countries in Asia, Africa and Europe. (AB 16.07)

Back to Table of Contents

5.14 Oman’s Latest Budget Update Reveals Deficit Narrowing

Downgraded by all three major rating companies and facing speculation whether a bailout might be needed, the sultanate stopped providing data on its budget performance this year. A monthly bulletin published by the central bank a week ago, which includes a breakdown of government revenue and expenditure, only covers a period through November 2018.

However, in a report dated 18 July, the National Centre for Statistics and Information said the deficit narrowed in the first five months of the year to 358.4 million rials ($931 million), down from 1.1 billion rials a year earlier.

In a region where investors have already expressed concern about the lack of economic statistics, Oman’s delay risked testing the market’s nerves. Its budget has been slow to heal after the oil rout five years ago, as the government lagged behind on fiscal reforms and ran an average deficit of 17% in 2015-2017. Although a rebound in crude prices brought some relief, S&P Global Ratings estimates last year’s shortfall at 8.9% of gross domestic product, more than 1% higher than it initially projected, a result of spending increases and underperformance in non-hydrocarbon revenue.

The International Monetary Fund sees the shortfall narrowing over the next several years before it begins to climb back up from 2022, according to a July report. Oman’s state budget plan envisaged a deficit of 9% for this year, or 2.8 billion rials, slightly more than last year’s actual deficit of 2.65 billion rials. Budget revenue in January-May 2019 rose more than 15% from a year earlier, while spending dropped 4.3%, according to the statistics service.

Oman, which S&P estimates relies on hydrocarbons for 70% of its fiscal receipts, has started to make some headway, imposing an excise tax that could generate close to 100 million rials in annual revenue. But even as the sultanate succeeded last year in bringing down its current-account deficit by over 10% of GDP, its government debt continued to increase, according to the IMF, which also cut its estimate for Oman’s economic growth in 2019 to near zero. (AB 22.07)

Back to Table of Contents

5.15 IMF Urges Oman to Introduce VAT as Soon as Possible

The International Monetary Fund has urged Oman to introduce VAT as soon as possible as the sultanate’s economic recovery from the 2014 oil price shock remains subdued. The UAE and Saudi Arabia were the first countries in the GCC to introduce a 5% VAT on 1 January 2018 while Bahrain made the move a year later, but Oman, Kuwait and Qatar have not yet implemented the tax. While welcoming the Oman’s plans to continue with fiscal consolidation, IMF directors called for an expeditious introduction of VAT and measures to adjust government spending. They also encouraged Omani authorities to implement an ambitious medium-term fiscal adjustment plan, based on reforms to tackle current spending rigidities, streamline public investment and raise non-hydrocarbon revenue. The recommendations were made by the executive board of the IMF following the conclusion of an Article IV consultation with Oman.

The IMF said since the 2014 oil price shock, Oman’s policy efforts have aimed at strengthening the fiscal position, enhancing private sector-led growth and employment, and encouraging diversification. It added that economic activity started to recover last year, and the overall fiscal and current account deficits improved somewhat, reflecting mainly higher oil prices. However, macroeconomic vulnerabilities continued to rise, with government and external debt increasing further, while some fiscal reforms were delayed. Higher vulnerabilities have led to new sovereign credit rating downgrades and increases in sovereign risk premiums.

The IMF said economic activity is gradually recovering in Oman with estimates that, after reaching a low of 0.5% in 2017, real non-hydrocarbon GDP growth has increased to about 1.5% last year, reflecting higher confidence driven by the rebound in oil prices. Furthermore, oil and gas production increases boosted hydrocarbon GDP growth in 2018 to an estimated 3.1%, the IMF said, adding that these developments brought overall real GDP growth to 2.2%. Non-hydrocarbon growth is projected to increase gradually over the medium term, reaching about 4%, assuming efforts to diversify the economy continue. Preliminary budget execution data indicates an improvement in the overall fiscal balance last year with a fiscal deficit estimated to have declined to about 9% of GDP from 13.9% of GDP in 2017.

IMF executive directors welcomed steps taken over the past few years to enhance private sector growth, reduce spending growth, diversify government revenue, and improve the business environment but called for a deeper fiscal adjustment to maintain confidence and ensure fiscal and external sustainability. Directors concurred that the exchange rate peg to the US dollar had delivered low and stable inflation and remained appropriate. (AB 12.07)

Back to Table of Contents

5.16 Saudi Arabia Raises Price of Petrol

Saudi state oil company Saudi Aramco on 14 July announced a 3.8% increase in prices for Octane 95 gasoline from SR 2.10 last quarter to SR2.18 and for Octane 91 from SR1.44 to SR1.53 per liter. The world’s largest exporter of crude oil said domestic gasoline prices are subject to fluctuations due to changes in export prices to global markets. Despite OPEC partners restricting oil production, the kingdom recently awarded $18 billion in 34 contracts (half of them going to Saudi firms) to boost output capacity at two offshore deposits. The company will add a total 550,000 barrels a day of capacity at its Marjan and Berri oil fields. It did not, however, identify the 16 companies that won the contracts or specify when the projects would be completed. Saudi Aramco regularly produces 10 million barrels a day, but aims to produce 12 million daily in a bid to maintain spare capacity available for quick use in case of shortages. (AB 15.07)

Back to Table of Contents

►►North Africa

5.17 Egypt’s Inflation Rate Drops for the First Time in 2019

Egypt’s annual urban consumer price inflation fell sharply to 9.4% in June from 14.1% in May, CAPMAS announced on 10 July, a significantly bigger drop than analysts had expected. CAPMAS revealed also that the inflation rate, on an annual basis, declined during the past June to reach 8.9% compared to the same time in 2018 which had recorded 13.8%. It added that the inflation rate recorded 12.4% during the first half of 2019. Pundits said the deceleration was partly due to last year’s high base effect and lower vegetable prices, which are often a key contributor to high inflation.

Urban inflation fell month-on-month in June by 0.8% after rising by 1.1% in May, the statistics showed. Vegetable prices rose 17.6% year-on-year in June, but fell 10% compared to May. Egypt raised fuel prices last week by between 16% and 30% as part of an IMF-backed economic reform program that saw inflation rise to a high of 33% in 2017. While economists had predicted a softer deceleration in inflation in June, most continued to predict the bank would hold rates until the fuel price hikes’ impact is tested. (CAPMAS 10.07)

Back to Table of Contents

5.18 Egypt’s Trade Balance Deficit Hits $3.87 Billion in April 2019